A loan-to-value (LTV) ratio compares the amount of debt required to purchase a home to the value of the house being purchased.

LTV is important because it is used by lenders to assess whether or not to grant a loan and/or what terms to offer a borrower. The larger the LTV, the greater the lender's risk—if the borrower defaults, the lender is less likely to recoup their investment by selling the home.

The loan-to-value ratio is a straightforward computation that compares the amount of money borrowed to buy an object to its value. It also displays how much equity a borrower has in the home used to secure the loan—how much money would be left over if the borrower sold the home and paid off the debt.

The LTV is the reverse of the down payment made by the borrower. For example, a borrower with a 20% down payment has an LTV of 80%.

What constitutes a good LTV varies depending on the type of asset being financed. When purchasing a home, an LTV of 80% or less is generally regarded as good—this is the limit you cannot surpass if you want to avoid paying mortgage insurance. Borrowers must make a down payment of at least 20%, plus closing fees, to obtain an 80% LTV.

While 80% is regarded as appropriate, conservative homeowners may prefer even lower LTVs to minimize monthly payments or qualify for better interest rates.

To calculate your loan-to-value, simply add the total amount borrowed against an asset. The total should then be divided by the appraised value of the property being financed.

It's also crucial to remember that the loan amount may include charges that lenders allow borrowers to finance rather than pay upfront at closing, such as loan document preparation and filing fees. However, because those expenses do not add to the property value, they improve your LTV.

Making a larger down payment when purchasing a home is one method for lowering your LTV. If you borrowed $400,000 with a $10,000 down payment, your LTV would be 97.5%. If the LTV surpasses 97%, a conventional loan cannot be acquired. As a result, you'd need to put down at least $12,000 to increase your LTV to 97%.

Another way to minimize your LTV when buying a property is to choose a less expensive residence. Putting down $10,000 on a $300,000 house instead of a $400,000 house results in an LTV of approximately 97%.

Paying down your loan's principal reduces your LTV. If the value of your home rises, your LTV will decrease.

To get approved for a home loan, it's best to plan on putting down at least 20% of the home's value—this would result in an LTV of 80% or less. If your LTV reaches 80%, your loan may be denied or you may be required to acquire mortgage insurance to be approved.

LTV is also crucial because if you're buying a home and the appraised value is significantly lower than the purchase price, you may need to make a higher down payment so that your LTV doesn't exceed your lender's limitations.

If you currently own a house and are considering a home equity line of credit (HELOC), most lenders will allow you to borrow up to 90% of the value of your home when paired with your existing mortgage. If the value of your home has dropped since you bought it, you may be unable to obtain a home equity loan or HELOC.

Assume you own a $100,000 home that you purchased five years ago. Your current LTV is 65% if you have a mortgage with a balance of $65,000. If your credit is good and you qualify for additional financing, you may be able to borrow up to $25,000 through a HELOC, increasing your total LTV to 90%.

Finally, if you already have a loan and your house value declines to the point where your LTV exceeds your lender's limits, most home loans aren't callable, which means the lender can't demand repayment before the loan term expires. However, some HELOCs are. Alternatively, if the term of your HELOC is about to expire, your lender may opt not to renew it. If you have a balloon mortgage, you may encounter difficulties refinancing your balloon payment at the end of your loan.

While a loan-to-value ratio considers the amount borrowed against a home about its value, combined LTV considers the total amount borrowed against the value of a home across multiple loans.

This is essential because, in contrast to many lenders, combined LTV includes the total amount borrowed in any loan secured by the property, including first and second mortgages, home equity lines of credit, and home equity loans.

Loan-to-Value Requirements for Various Mortgage Types

Every lender and loan type has its own set of constraints and restrictions, including the LTVs of borrowers. Some even have two thresholds—for example, an absolute limit and a minimum required to avoid additional protections like mortgage insurance.

Traditional Loans

Conventional mortgages follow lending guidelines established by government-sponsored enterprises such as Fannie Mae and Freddie Mac. These loans comprise the great majority of all mortgages issued in the United States. Lenders set a limit LTV of 80% on traditional mortgages for borrowers who want to avoid acquiring private mortgage insurance. Borrowers who are prepared to acquire mortgage insurance may be able to get up to 97% LTV if the lender improves.

Mortgages Guaranteed By The FHA

The Federal Housing Administration makes FHA loans directly to homeowners. These loans are specifically designed to encourage homeownership among borrowers who would be unable to afford a down payment on a regular loan. The maximum loan-to-value ratio for FHA loans is 96.5%.

It's also worth noting that all FHA loans require borrowers to purchase mortgage insurance as part of the loan program, so greater down payments don't save homeowners money.

VA Loans

VA loans are government-backed mortgages intended exclusively for members of the United States military and veterans. Eligible borrowers can finance up to 100% of a home's worth through VA loan programs. Borrowers are often still responsible for paying any fees and other closing costs that, when combined with the purchase price, exceed the home's value.

USDA Loans

USDA loans are government-backed loans granted directly by the United States Department of Agriculture. Department of Agriculture and are intended to assist rural residents in affording homeownership. Home purchasers can finance up to 100% of the purchase price of an existing home using the USDA's home loan programs. For existing home loans, the USDA will frequently cover "excess expenses" (those that exceed the home's worth), such as:

For more content like this, visit our website today!

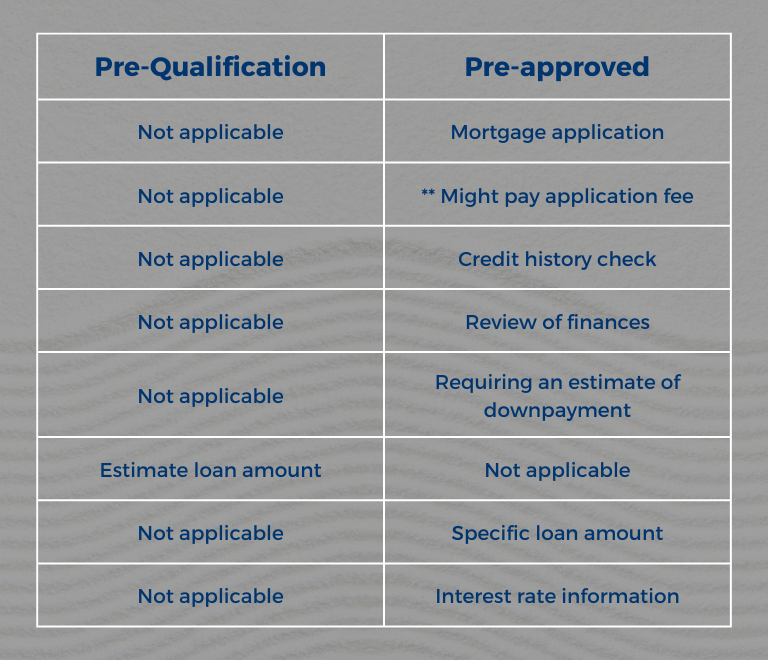

If you happen to apply for a loan or mortgage you might encounter new terms, such as pre-qualifying and pre-approval. It’s no surprise though since these are the key steps in processing your application. People might use these terms conversely, but there are important differences that applicants must understand.

Pre-qualification is the first step in loan application. During this process, the borrower provides the lender with an overview of their financial capability, including their income, assets, and debt. This will help the lender create an estimate of how much can be borrowed.

Pre-approval is the second step. This is a conditional commitment that often tells the borrower that they are qualified for the amount they’re applying for. This process usually takes longer than the initial step.

The difference between the two? Getting pre-qualified is much faster and the details are not that much while the pre-approvals are more comprehensive.

Nonetheless, pre-qualified or pre-approval doesn’t mean that having these letters can secure you a loan from the lenders you are applying for. However, having these may help you prove that you are capable of buying and purchasing a home.

As mentioned, this is an early step in the application process. During this time, the borrower submits financial data for the lenders to review. Getting pre-qualified means providing the lender will look at your overall financial picture. It includes your current and past debts, income, businesses, assets, bank account information, and your ideal loans and payment amounts.

They will also look and review whether you can pay on time. During pre-qualification, they will give an estimate of how much you are allowed to borrow and will give you different options that are available to you. This is known as a soft inquiry and will not affect your credit score.

Pre-qualification process as mentioned, doesn’t require detailed information and doesn’t ask for statements or other detailed financial information as required in the pre-approval process. Processing pre-qualification can be done online or over the phone. It will also not involve any amount.

Pre-qualification is fast and won’t take a week to process, but remember that pre-qualification doesn’t include credit reports being reviewed or an in-depth look at the borrower’s capacity to purchase. The initial pre-qualification is for discussion of any needs regarding your application for a loan or mortgage. Lenders will discuss options that you can have and what suits you best.

Then again, this is not a guarantee that you will get a loan. It will just be based on the information you have given or provided, and will only give you the possible amount you can borrow or expect. It’s not the same weight as the pre-approval that has more detailed requirements and thorough investigation.

Getting pre-approved is the next step after the pre-qualification. Pre-approval is a much longer process and requires a more detailed investigation. They will look through your financial information and your credit history report. When you have a pre-approved letter, it’s a good indication that you are creditworthy and that you can borrow.

A complete official application form is needed to get pre-approved. By providing lenders with the necessary documents, they can run and perform an extensive financial background check and will give you a more precise estimate of how much the lender is willing to lend allowing borrowers to look for homes or cars lower than the price level. It puts borrowers at an advantage, such as having a better interest rate.

Unlike pre-qualification, pre-approvals require hard inquiry, which can affect and temporarily lower your credit score. It also takes longer and may take up to 10 days.

As mentioned above, pre-qualification only gives an estimated amount of what you can loan based on the information you have provided, and believe that you will qualify for a loan. Getting pre-approved, on the other hand, has more detailed information about your financial information and loans you the money for a mortgage.

What are the advantages of completing both steps? It gives an idea of how much a borrower can spend. For example, when you are looking for a home, you will save time and effort by looking for homes that are within your budget instead of houses that are too expensive. If you’re pre-approved, it can help speed up the buying process, letting the seller know that you’re serious about getting the house. Most sellers are more willing to negotiate with those who are pre-approved, allowing borrowers to get and close a home more quickly.

After you have made it to the two steps, the borrower will give a copy of the purchase agreement to the lender. Aside from the purchase agreement, other necessary documents should also be given to the lender as a part of the full underwriting process after you have made an offer. Lenders will hire a licensed contractor to do a home appraisal and determine the home’s value. Loan commitment will be the final step in the process. A loan commitment is an agreement by banks and other financial institutions to lend an individual a sum of money. This is only issued by the bank when approved.

You don’t have to spend all the money on the pre-approved amount. It is ideal to spend less. Depending on the market and the home you choose, you can spend less money leaving you with an extra budget that you can use for other expenses like emergencies, renovations, or for future use. Checking your entire budget can help you determine what will work for you and your financial situation.

Pre-qualified and pre-approved have different meanings. However, these are both essential steps in the loan or mortgage process. Pre-qualification indicates the estimated amount that you can get when you take the loan and pre-approved has a more thorough investigation, a commitment with conditions from lenders that you will be approved for a mortgage. Knowing the difference between the two can help you go smoothly in the process.