If you happen to apply for a loan or mortgage you might encounter new terms, such as pre-qualifying and pre-approval. It’s no surprise though since these are the key steps in processing your application. People might use these terms conversely, but there are important differences that applicants must understand.

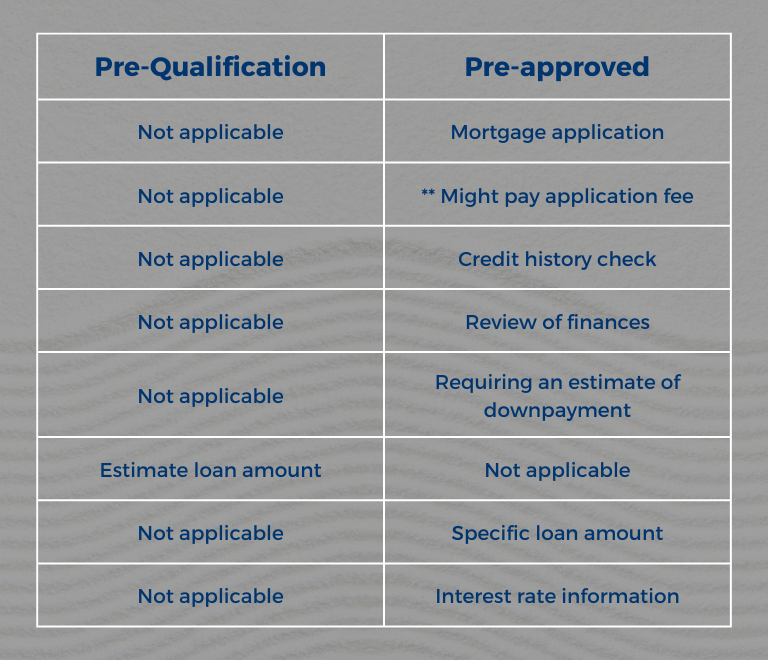

Pre-qualification is the first step in loan application. During this process, the borrower provides the lender with an overview of their financial capability, including their income, assets, and debt. This will help the lender create an estimate of how much can be borrowed.

Pre-approval is the second step. This is a conditional commitment that often tells the borrower that they are qualified for the amount they’re applying for. This process usually takes longer than the initial step.

The difference between the two? Getting pre-qualified is much faster and the details are not that much while the pre-approvals are more comprehensive.

Nonetheless, pre-qualified or pre-approval doesn’t mean that having these letters can secure you a loan from the lenders you are applying for. However, having these may help you prove that you are capable of buying and purchasing a home.

As mentioned, this is an early step in the application process. During this time, the borrower submits financial data for the lenders to review. Getting pre-qualified means providing the lender will look at your overall financial picture. It includes your current and past debts, income, businesses, assets, bank account information, and your ideal loans and payment amounts.

They will also look and review whether you can pay on time. During pre-qualification, they will give an estimate of how much you are allowed to borrow and will give you different options that are available to you. This is known as a soft inquiry and will not affect your credit score.

Pre-qualification process as mentioned, doesn’t require detailed information and doesn’t ask for statements or other detailed financial information as required in the pre-approval process. Processing pre-qualification can be done online or over the phone. It will also not involve any amount.

Pre-qualification is fast and won’t take a week to process, but remember that pre-qualification doesn’t include credit reports being reviewed or an in-depth look at the borrower’s capacity to purchase. The initial pre-qualification is for discussion of any needs regarding your application for a loan or mortgage. Lenders will discuss options that you can have and what suits you best.

Then again, this is not a guarantee that you will get a loan. It will just be based on the information you have given or provided, and will only give you the possible amount you can borrow or expect. It’s not the same weight as the pre-approval that has more detailed requirements and thorough investigation.

Getting pre-approved is the next step after the pre-qualification. Pre-approval is a much longer process and requires a more detailed investigation. They will look through your financial information and your credit history report. When you have a pre-approved letter, it’s a good indication that you are creditworthy and that you can borrow.

A complete official application form is needed to get pre-approved. By providing lenders with the necessary documents, they can run and perform an extensive financial background check and will give you a more precise estimate of how much the lender is willing to lend allowing borrowers to look for homes or cars lower than the price level. It puts borrowers at an advantage, such as having a better interest rate.

Unlike pre-qualification, pre-approvals require hard inquiry, which can affect and temporarily lower your credit score. It also takes longer and may take up to 10 days.

As mentioned above, pre-qualification only gives an estimated amount of what you can loan based on the information you have provided, and believe that you will qualify for a loan. Getting pre-approved, on the other hand, has more detailed information about your financial information and loans you the money for a mortgage.

What are the advantages of completing both steps? It gives an idea of how much a borrower can spend. For example, when you are looking for a home, you will save time and effort by looking for homes that are within your budget instead of houses that are too expensive. If you’re pre-approved, it can help speed up the buying process, letting the seller know that you’re serious about getting the house. Most sellers are more willing to negotiate with those who are pre-approved, allowing borrowers to get and close a home more quickly.

After you have made it to the two steps, the borrower will give a copy of the purchase agreement to the lender. Aside from the purchase agreement, other necessary documents should also be given to the lender as a part of the full underwriting process after you have made an offer. Lenders will hire a licensed contractor to do a home appraisal and determine the home’s value. Loan commitment will be the final step in the process. A loan commitment is an agreement by banks and other financial institutions to lend an individual a sum of money. This is only issued by the bank when approved.

You don’t have to spend all the money on the pre-approved amount. It is ideal to spend less. Depending on the market and the home you choose, you can spend less money leaving you with an extra budget that you can use for other expenses like emergencies, renovations, or for future use. Checking your entire budget can help you determine what will work for you and your financial situation.

Pre-qualified and pre-approved have different meanings. However, these are both essential steps in the loan or mortgage process. Pre-qualification indicates the estimated amount that you can get when you take the loan and pre-approved has a more thorough investigation, a commitment with conditions from lenders that you will be approved for a mortgage. Knowing the difference between the two can help you go smoothly in the process.